LTD on your paystub stands for Long-Term Disability insuranceInsurance that provides income replacement for individuals who are unable to work for an extended pe..., a payroll deduction that funds an income replacement policy if a serious illness or injury keeps you out of work for months or years. Most group LTD plans replace 50% to 70% of your pre-disability earnings after a 90 to 180-day waiting period, and the line appears as LTD, LTD EE, LTD ER, or VOL LTD depending on who pays the premium. The Social Security Administration estimates that 65% of the private sector workforce has no long-term disability insuranceA form of insurance that provides income to individuals who are unable to work due to a disability.. If your paystub shows this line, you have a financial safety net that most workers do not.

This guide breaks down what LTD means line by line, how the premium is split between you and your employer, how benefits are calculated and taxed, and how LTD interacts with Social Security Disability Insurance (SSDI)A U.S. government program that provides financial assistance to individuals who are unable to work d... if your condition lasts long enough to qualify for both. For a closer look at the dollar amount you would actually receive, see our guide on how much long-term disability pays.

Key Takeaways

- LTD payroll code: LTD on a paystub is your Long-Term Disability insurance premium, funding income replacement if injury or illness keeps you out of work past short-term disability.

- Standard payout: Most group LTD policies pay 50% to 70% of pre-disability earnings, starting after a 90 to 180-day elimination period.

- Premium cost: LTD insurance typically costs between 1% and 3% of an employee's annual salary, with employers often paying part or all of it.

- Tax rule that matters most: If your employer paid the premium with pre-tax dollars, LTD benefits are fully taxable; if you paid with after-tax dollars, benefits are 100% tax-free.

- LTD versus SSDI: LTD is private insurance, and SSDI is a federal program. You can receive both, but most LTD policies offset (reduce) your payment by your SSDI award.

- Read the SPD before you need it: Your Summary Plan Description defines elimination period, benefit cap, offset rules, and 'own occupation' versus 'any occupation' standards.

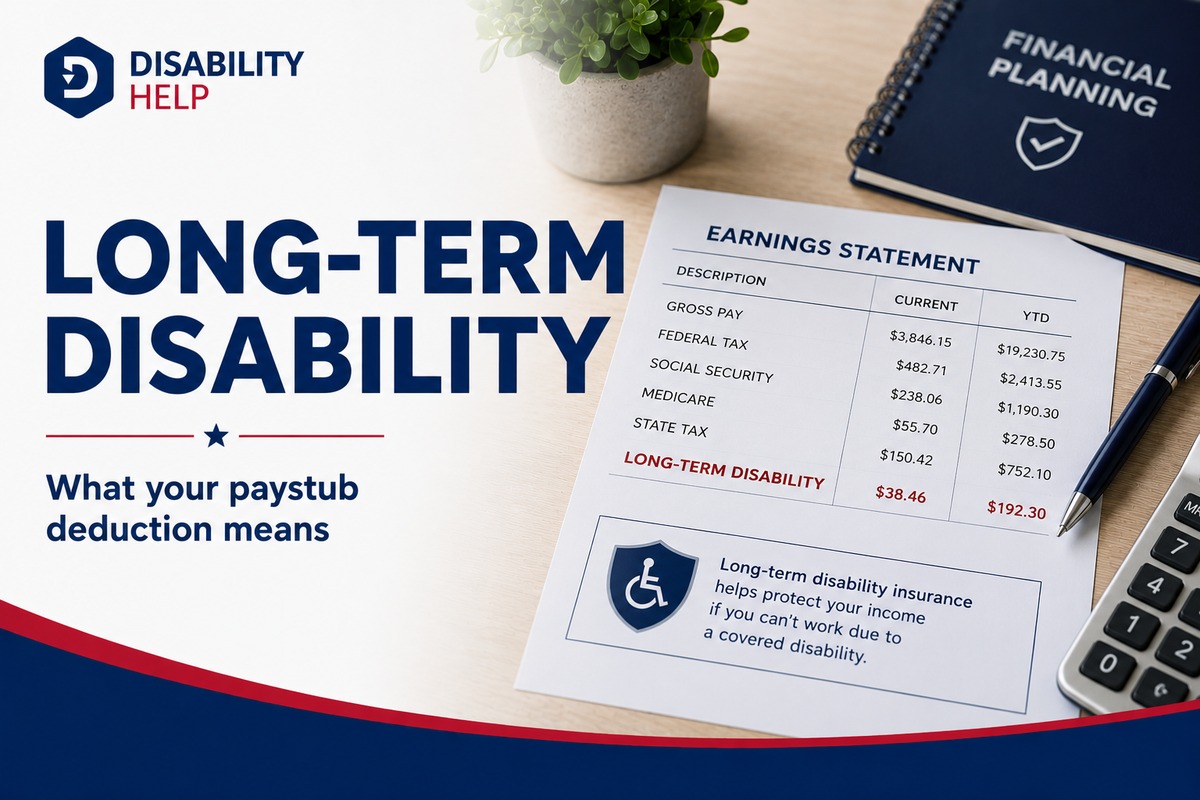

What Does LTD Mean on Your Paystub?

LTD stands for Long-Term Disability insurance. The deduction on your paystub is the premium your employer (or both of you together) pays to keep you covered if a non-work-related illness or injury keeps you out of work for an extended period. This is private insurance, not a government program, and it is separate from SSDI even though both pay income to disabled workers.

Long-Term Disability is the largest piece of most workplace disability protection plans. According to ADP, the average length of LTD coverage is two to five years per claim, though some policies pay out until age 65 or full retirement age. The benefit kicks in only after you exhaust short-term disability or wait through an elimination period of 90 to 180 days, whichever your policy specifies, though your plan may use a different waiting period.

If you have never filed a claim, the LTD line on your paystub may feel like one more deduction, taking a small bite out of each check. The Social Security Administration estimates that about 65% of the private sector workforce has no long-term disability insurance at all, making this benefit one of the most underused but most valuable lines in a worker's pay statement.

How LTD Appears on Your Paystub: LTD, LTD EE, LTD ER, and VOL LTD

You will see LTD on your paystub in one of four common forms, and each tells you something different about who is paying and what kind of coverage you have. The codes look small, but they have direct tax consequences if you ever file a claim.

- LTD: A general code showing the basic Long-Term Disability deduction without identifying who pays. Often used when the employer fully covers the premium and tracks the cost for informational purposes only.

- LTD EE: Your share of the premium. 'EE' stands for Employee. This is money taken out of your paycheck each pay period.

- LTD ER: The employer's share. 'ER' stands for Employer. Shown for transparency, this amount is paid by the company on your behalf and does not reduce your gross pay.

- VOL LTD: Voluntary Long-Term Disability. You opted into this coverage during open enrollment, usually on top of a basic employer-paid plan, and you pay the full premium yourself, often with after-tax dollars.

The split between LTD EE and LTD ER matters more than most workers realize. Whoever pays the premium determines whether your future benefits are taxable, which we cover in the tax section below.

How Much Does LTD Insurance Pay?

Most group LTD policies pay between 50% and 70% of your pre-disability gross monthly earnings, capped at a maximum monthly benefit set in your policy. If you earn $5,000 per month and your policy replaces 60%, your monthly LTD benefit would be $3,000.

The actual calculation depends on three factors:

- Your income replacement rate, usually 50% to 70%.

- Your pre-disability earnings, which may or may not include bonuses, commissions, and overtime depending on the policy.

- The monthly cap, which can range from $4,000 to $25,000 per month under most group plans, according to legal publisher Nolo.

Some policies also include a cost-of-living adjustment (COLA) rider that increases your benefit by 1% to 3% each year to keep pace with inflation. For a deeper look at how the monthly payment is calculated, see Disability Help's guide on how much long-term disability pays.

Once you start drawing benefits, the insurer will require periodic medical updates, usually every three to twelve months, to confirm you still meet the policy's definition of disability. Failing to provide that documentation can end your benefits even if your condition has not changed.

Who Pays the LTD Premium, and What Does It Cost?

Premium responsibility varies by employer, and the structure directly affects what you see on your paystub. Long-Term Disability insurance generally costs between 1% and 3% of an employee's annual salary. For group plans, employers typically pay $0.25 to $0.75 per $100 of covered payroll, which works out to roughly $15 to $50 per employee per month.

Here is how the three common premium structures compare:

| Premium structure | Who pays | What you see on paystub | Effect on benefits if you file a claim |

|---|---|---|---|

| Employer-paid (fully funded) | Employer covers 100% | No LTD deduction (LTD ER may appear for info) | Benefits 100% taxable |

| Employee-paid (after-tax) | You pay 100% from take-home pay | LTD EE or VOL LTD shown as deduction | Benefits 100% tax-free |

| Shared cost | Employer and employee split | Both LTD EE and LTD ER appear | Partially taxable, proportional to the employer share |

The premium split is not just an accounting detail. Many financial advisors recommend choosing employee-paid after-tax LTD when offered, because the tax-free benefits keep more money in your pocket if you ever need them.

Are LTD Benefits Taxable? The IRS Rule You Need to Know

Whether LTD benefits are taxed depends entirely on who paid the premium and how it was paid. The IRS has been clear on this point: the same dollar gets taxed once, either when the premium is paid or when the benefit is received.

According to official IRS guidance on disability insurance proceeds, if your employer paid the premium and did not include the cost as taxable income on your W-2, the benefits are fully taxable when you receive them. If you paid the premium with after-tax dollars from your paycheck, the benefits are tax-free.

| Premium payment method | Are LTD benefits taxable? | Reported on |

|---|---|---|

| Employer pays 100% (pre-tax) | Yes, 100% taxable | W-2 or 1099 |

| Employee pays through cafeteria plan (pre-tax) | Yes, fully taxable | W-2 or 1099 |

| Employee pays with after-tax dollars | No, 100% tax-free | Not reported as income |

| Shared cost | Partially taxable, proportional to employer share | W-2 or 1099 |

Example: if your employer paid 60% of the premium and you paid 40% with after-tax dollars, 60% of your LTD benefit would be taxable when you file your return.

This rule has a practical consequence for anyone making coverage decisions during open enrollment. Choosing the slightly more expensive employee-paid option can mean thousands more dollars in your pocket each year if you ever file a claim. Talk to your HR department or a tax professional before making the switch.

LTD vs. STD vs. SSDI: How the Three Benefits Connect

LTD does not stand alone. Most workers with serious illnesses or injuries move through a sequence of benefits, starting with paid leave and ending with federal disability if their condition meets SSA standards. Understanding the order helps you avoid gaps in income.

| Feature | Short-Term Disability (STD) | Long-Term Disability (LTD) | Social Security Disability (SSDI) |

|---|---|---|---|

| What it is | Private insurance | Private insurance | Federal program |

| Income replacement | 60 to 70% of pay | 50 to 70% of pay | Based on lifetime earnings |

| Waiting period | 7 to 14 days | 90 to 180 days | 5 months |

| Duration | 3 to 6 months | 2 years to age 65 | Until recovery or retirement |

| Average benefit | Varies by policy | Up to $10,000/month cap typical | $1,633/month (Jan 2026 SSA average) |

| Source | Employer-sponsored | Employer-sponsored or individual | SSA, funded by payroll taxes |

According to Congressional Research Service data, about 8.1 million people received SSDI benefits in January 2026, with the average disabled-worker payment at roughly $1,633 per month. SSDI alone replaces a far smaller share of pre-disability income than most LTD policies, which is one reason workers benefit from having both.

If your disability lasts longer than 12 months, most LTD policies actually require you to apply for SSDI. When the SSA approves your claim, your LTD insurer will offset its payment by the amount of your SSDI benefit, so your total monthly income stays roughly the same. The offset is not optional and is written into nearly every group LTD contract.

For caregivers and authorized representatives helping someone apply for both, see our guide on how to qualify for SSDI benefits and our overview of collecting short-term disability and Social Security at the same time.

Common Misconceptions and Surprises About LTD Claims

Many workers assume that having LTD coverage means easy approval if they ever need to use it. The reality is more complicated. Below are five of the most common myths that catch claimants off guard.

- "A doctor's note proves I cannot work." LTD insurers require extensive medical documentation, functional capacity evaluations, and ongoing diagnostic evidence. A note from your physician is rarely enough on its own.

- "Benefits run until retirement once approved." Many policies cap mental health and cognitive disorder claims at 24 months, even if the condition continues. Insurers also conduct periodic reviews and can end benefits if they determine your condition has improved.

- "Winning SSDI guarantees my LTD claim." SSDI uses federal disability criteria, while private LTD policies use their own definitions. Approval from the SSA does not bind your insurer.

- "'Own occupation' applies forever." Most policies start with an 'own occupation' definition for the first 24 months, then switch to 'any occupation,' a stricter standard that requires you to be unable to perform any job you are reasonably suited for.

- "My LTD payment is mine to keep." Most policies contain an offset clause that reduces your LTD by the amount of any SSDI, workers' compensation, or pension income you receive. If you get an SSDI back-pay lump sum, the insurer can demand repayment of the LTD already paid to you.

These provisions are written in plain language inside your Summary Plan Description. If you cannot find your SPD, request a copy from HR before you need to file a claim, not after.

Key Terms Every LTD Participant Should Know

LTD policies use language that can feel foreign even to readers who have studied their benefits handbook closely. Knowing these terms before you file a claim makes the process less stressful.

Elimination period: The waiting time between when your disability begins and when LTD benefits start, usually 90 to 180 days.

Own occupation: A policy definition under which you are disabled if you cannot perform the duties of your specific job, usually applied during the first 24 months of a claim.

Any occupation: A stricter definition that activates after 24 months, requiring that you cannot perform any job for which your education, training, or experience reasonably qualifies you.

Offset: The amount your LTD insurer subtracts from your monthly payment to account for other income sources like SSDI, workers' comp, or a pension.

Cost of living adjustment (COLA): An optional rider that increases your benefit by 1% to 3% per year to keep pace with inflation.

Pre-disability earnings: The income figure used to calculate your benefit, usually your gross monthly salary right before you became disabled.

Summary Plan Description (SPD): The official document that explains your specific policy, including elimination periods, benefit caps, exclusions, and offset rules.

Expert Insight: Why Premium Tax Choices Matter More Than the Premium Itself

The Patient Advocate Foundation, a national 501(c)(3) nonprofit that assists patients with chronic illnessA long-term health condition that requires ongoing management, such as diabetes or multiple sclerosi..., advises workers to view LTD insurance not as a static benefit but as a financial planning decision. As the foundation notes in its guidance on long-term disability, if an LTD plan is offered through your employer, it is important to sign up during the initial enrollment period when you cannot be denied coverage for a pre-existing condition.

The lesson for workers reviewing their paystubs is this: the LTD line is not a place to look for savings. If the deduction is small, that is the price of a safety net that protects your largest financial asset, your ability to earn income. If your employer offers a choice between pre-tax and after-tax premium payment, choosing after-tax can convert taxable future benefits into tax-free income, which is often worth more than the small premium savings.

If your employer changes its LTD plan or you switch jobs, review the new policy's definition of disability, elimination period, benefit cap, and offset rules carefully. Those four items determine whether the coverage will actually replace your income when you need it. Workers who are already weighing a claim should also read our guide on transitioning from short-term to long-term disability benefits, which covers timing, documentation, and the gap-coverage issue most claimants face.

What to Do With This Information

The LTD line on your paystub is one of the most valuable benefits the average worker overlooks. As of 2026, about 90% of workers aged 21 to 64 who paid into Social Security qualify for SSDI in the event of a severe disability, according to SSA estimates. SSDI replaces only a portion of pre-disability income, which is why pairing it with LTD coverage is the standard approach for workers who want true income protection.

Before your next open enrollment, pull up your Summary Plan Description and check four things: the elimination period, the income replacement rate, the maximum monthly benefit, and whether the premium is paid pre-tax or after-tax. If your employer offers a choice, the after-tax option usually produces a better outcome if you ever need the benefit.

If your disability is already affecting your ability to work and you are considering an LTD claim, Disability Help's guide on transitioning from short-term to long-term disability benefitsFinancial assistance provided to individuals who are unable to work due to a disability, such as Soc... walks you through the documentation, employer communication, and timing steps that protect your claim. The earlier you understand the policy on your paystub, the more options you have when the benefit actually matters.

Need help understanding what happens after LTD begins?

Long-term disability can affect your income, health coverage, SSDI claim, and other benefits. For a practical next step, read Disability Help’s guide on who pays health insurance while you’re on long-term disability, so you can plan for both your paycheck and your medical coverage before a claim disrupts either one.

Frequently Asked Questions

What does LTD on my paystub mean?

LTD on your paystub is a payroll deduction for Long-Term Disability insurance. The premium funds a policy that replaces 50% to 70% of your pre-disability income if a non-work-related illness or injury keeps you out of work past your short-term disability period, usually 90 to 180 days.

Is LTD the same as SSDI?

No. LTD is private insurance offered through your employer or purchased individually. SSDI is a federal program administered by the Social Security Administration and funded through payroll taxes. You can receive both at the same time, but your LTD insurer will likely reduce its payment by the amount of your SSDI benefit through an offset clause.

Are my LTD benefits taxable in 2026?

It depends on who paid the premium. If your employer paid with pre-tax dollars, your benefits are 100% taxable as ordinary income. If you paid with after-tax dollars from your paycheck, your benefits are 100% tax-free. Shared premium plans produce partially taxable benefits proportional to the employer's share. See the IRS rules on disability insurance proceeds for the official guidance.

How much does LTD insurance cost per paycheck?

LTD premiums generally cost between 1% and 3% of your annual salary. For a worker earning $60,000 per year, that translates to roughly $600 to $1,800 annually, or about $25 to $75 per pay period if you are paid twice a month. Employers often cover part or all of the premium.

Can my employer cancel my LTD coverage?

Yes. LTD is a benefit, not a legal right, and most employers can change or end the plan at open enrollment. If you leave the job, your group LTD coverage typically ends, although some policies offer conversion to an individual plan. Ask HR about conversion options before you leave.

What happens to my LTD if I get approved for SSDI?

Most LTD policies require you to apply for SSDI once your disability is expected to last at least 12 months. When the SSA approves your claim, your LTD insurer will offset its monthly payment by the amount of your SSDI award. If you receive an SSDI back-pay lump sum, the insurer may require you to repay the LTD overpayment that resulted.